China’s dominance across the lithium-ion battery supply chain, spanning from raw material mining and processing to final battery production, risks locking the EU into a new form of energy dependence as it races to meet its European Green Deal targets.

Key takeaways:

-

The EU is dependent on China for three out of five critical raw materials needed for battery production, as well as for battery anodes and final lithium-ion batteries, where China accounts for over 80% of EU imports.

-

Despite having sufficient domestic manufacturing capacity, the EU cannot compete economically – battery production in Europe costs almost 50% more than in China, which poses significant barriers to entry for EU producers, as illustrated by the bankruptcy of Northvolt, the EU’s flagship battery maker, in 2024.

-

Unless the EU addresses its battery supply chain dependencies, its Green Deal ambitions are at risk – a supply disruption would leave the bloc unable to guarantee a sufficient supply of batteries for EVs and energy storage, stalling its transition away from fossil fuels.

Driven by electrification, the importance of batteries has increased dramatically in recent years. Used in the transport and energy sectors, lithium-ion batteries (the primary battery technology) are a central component of the global energy system. As such, a reliable and resilient battery supply chain is critical for the EU’s clean energy transition.

However, the battery supply chain is highly concentrated, with China holding a dominant position in several stages. China’s market share is especially pronounced in the manufacturing of intermediate components and in final battery production. Moreover, six of the ten largest EV battery makers in 2024 are Chinese, with giants CATL and BYD accounting for more than 50% of the market share. With increasing demand for batteries to successfully decarbonize, the current global distribution of the battery supply chain thus poses a vulnerability to the EU.

While trying to meet its ambitious European Green Deal goals, the EU risks becoming further dependent on Beijing. Import dependence of a product, as defined by MERICS, consists of three conditions: the EU’s imports of a product being double its exports; China accounting for more than 30% of all EU imports of a product; and the concentration of suppliers of a product being 2500 or higher on the Herfindahl–Hirschman Index (HHI), a standard measure of market concentration in a given industry. A potential dependence on China for batteries or other supply chain components would entail the EU relying on a strategic adversary and thus being unable to guarantee a sustainable supply of batteries to meet its green transition objectives.

Anatomy of the battery supply chain

The basic unit of a battery is the battery cell, which contains a cathode and an anode, both composed of several raw materials. Although the materials in specific lithium-ion battery chemistries vary, the most common chemistries generally depend on some combination of five critical raw materials: lithium, cobalt, manganese, nickel and graphite. These materials account for about 50–70% of the battery’s final cost. Several battery cells comprise battery modules, which are contained in a battery pack. Therefore, the battery supply chain consists of multiple stages, including the mining and processing of raw materials, the manufacturing of battery components, and the final production of batteries.

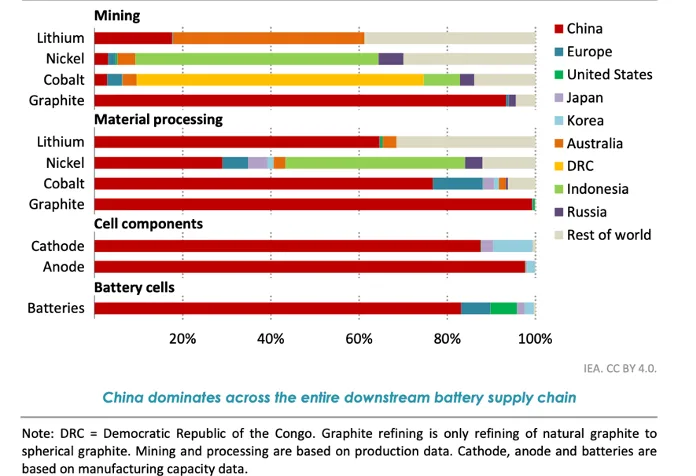

In 2023, China held a dominant position across the battery supply chain, accounting for more than 80% of global manufacturing capacity in the mid- and downstream stages, as well as more than 90% of global mining and processing capacity for graphite (Figure 1). It also accounted for a majority of the global lithium, manganese and cobalt processing capacity. Such global dominance poses significant challenges for countries to diversify their supplies, giving China the power to exert economic coercion on dependent countries.

Figure 1 – Geographical distribution of the global battery supply chain (Source: IEA, “Batteries and Secure Energy Transitions.”)

Mining and processing of raw materials

China’s strong presence at this stage of the battery supply chain, particularly in the processing of raw materials, results in considerable EU dependencies (Table 1). The EU is dependent on China for processed lithium and manganese, as well as for graphite supply. As such, it is dependent on China for three of the five raw materials needed for battery production. Moreover, in six analyzed products (lithium oxide and hydroxide, manganese dioxide, articles of manganese, cobalt oxides and hydroxides, other natural graphite, and artificial graphite), China’s share of EU imports is higher than 50%, although not all are dependent products. Lastly, several products appear highly concentrated, highlighting a lack of diversification options.

Although the EU is not dependent on China for the supply of extracted raw materials, apart from graphite, it is important to note that critical materials mined abroad are often exported to China for further processing because of China’s dominant share of global processing capacity. Moreover, Chinese companies also hold substantial stakes in foreign mining companies. Lastly, rather than through direct imports, raw materials often enter the EU embedded in clean technologies, including batteries, which is the primary source of the EU’s exposure.

Manufacturing of intermediate components

Cathode manufacturing is a highly concentrated market, with China accounting for around 90% of the global capacity. However, since global cathode manufacturing capacity (3.7 TWh) greatly exceeds global demand (0.9 TWh), China’s share of global production is slightly lower. In 2023, China accounted for around 80% of global cathode production, with the rest produced mostly in South Korea and Japan. The EU produced only 1 GWh of cathodes, while European demand reached about 68 GWh.

China’s presence in anode manufacturing is even more profound, accounting for 98% of the global capacity. However, similar to cathodes, the anode manufacturing capacity (7.3 TWh) significantly exceeds the global demand of 0.9 TWh. China accounted for roughly 90% of global anode production in 2023, followed by Japan and South Korea. The EU produced less than 1 GWh of anodes, with European demand being 71 GWh.

China’s dominance at this stage results in heavy EU dependence on anode imports from China, which account for more than 80% of European imports. On the contrary, despite China’s dominant share of global cathode manufacturing, the EU is not dependent on cathode imports from China, as the vast majority of cathodes (around 74%) are supplied by other Asia-Pacific countries.

Table 1 – EU dependence on China across the battery supply chain

Battery production

In 2023, China accounted for about 83% of global battery cell manufacturing capacity, followed by the EU and the US with around 6% each, corresponding to roughly 150 GWh. However, due to massive global overcapacity, utilization rates at battery cell production facilities were below 35% worldwide. In terms of actual production, China accounted for 75% of the global share in 2023. The EU produced around 67 GWh, which was less than half of the bloc’s demand. Table 1 shows that, despite having sufficient manufacturing capacity, the EU is heavily dependent on China for lithium-ion batteries, with China accounting for over 85% of the EU’s imports throughout 2023 and 2024.

One of the primary challenges to increasing lithium-battery production in the EU is the global production overcapacity. Global demand reached around 900 GWh in 2023, well below the global manufacturing capacity of almost 2600 GWh, which caused battery prices to fall. Given differences in capital costs for producing batteries worldwide, EU-based companies are undercut by cheaper production elsewhere, with battery production costs almost 50% higher in Europe than in China.

Moreover, the majority of the cost of battery manufacturing stems from the production of components and the associated material costs – the raw materials. China’s supply chain integration and dominant presence across the battery supply chain give it the upper hand over the EU, as it has access to raw materials at lower prices. The higher cost of production thus causes the EU to remain reliant on imports despite having sufficient manufacturing capacity.

It is also important to note that non-European battery manufacturers account for the vast majority of European production. This is unsurprising given the global market distribution – in 2024, the 10 biggest EV battery makers were all Chinese (6), South Korean (3) or Japanese (1). Around three-quarters of European production capacity is held by Korean companies, illustrating the lack of significant European battery makers. That is because, as a highly complex, low-profit-margin business, battery manufacturing confers an advantage on incumbent producers and creates significant barriers to entry for new producers. The case of the EU’s flagship battery manufacturer, Northvolt, which filed for bankruptcy in 2024, illustrates the difficulties accompanying entering the battery manufacturing market.

The dependency trap

China’s dominant presence across the battery supply chain results in significant EU dependencies. The EU is dependent on China for the processing and/or sourcing of three raw materials, anode manufacturing and final battery production. Such a dramatic level of dependence threatens the EU’s green transition goals and makes the Union vulnerable to economic coercion. In the event of a battery supply chain disruption, the EU would be unable to guarantee a sufficient supply of batteries for EVs and battery storage systems. This would slow the EU’s energy transition from fossil fuels, undermining both its decarbonization objectives and energy security.

Moreover, China’s dominance across the supply chain poses significant barriers to entry for potential EU-based producers, especially in stages with high overcapacity, such as cathode and anode manufacturing and battery production. This significantly complicates efforts to diversify supply and reduce the EU’s dependence on China.